Our mission is to provide superior risk-adjusted returns for Clifford Capital Partners clients so they can achieve their goals.

Quick Links

Philosophy

We believe our philosophy provides a time-tested foundation for our repeatable value investment discipline

Bottom Up

Thorough bottom up due diligence on every holding

Concentrated

Every name in the portfolio matters

High Conviction

Deep understanding of each business and risk

Benchmark Aware

Not benchmark driven

High Active Share

To outperform the benchmark, the portfolio must differ from the market.

Our Process

Investment Criteria

Core Value

Deep Value

Outside Clifford Criteria

Core Value

Deep Value

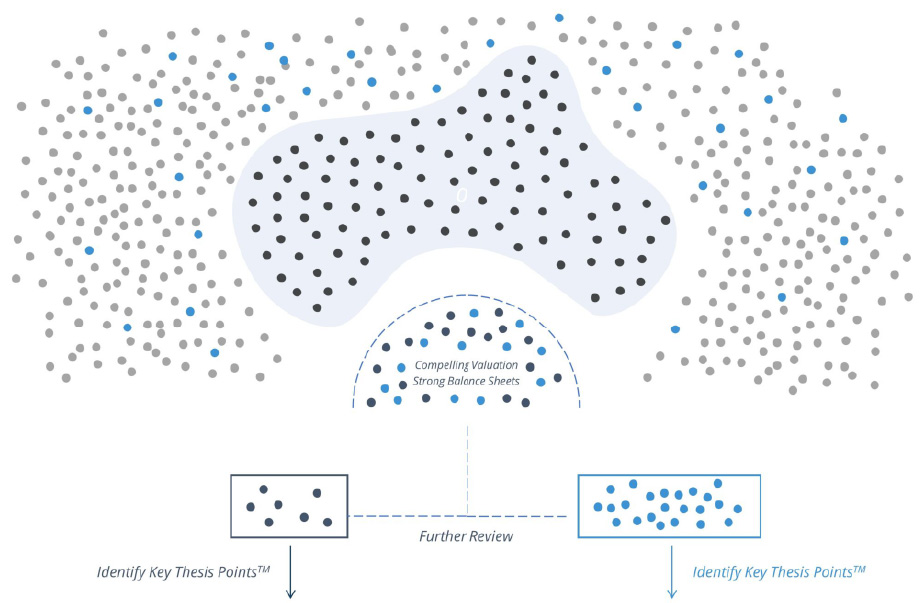

Through our proprietary Ten Point Review Process, we have pre-identified a short list of wide-moat businesses with high long-term financial return profiles, sustainable competitive advantages, and strong management teams.

Sometimes even the best companies in the US Stock Exchange are sold off by investors. If a Core Value name falls into our valuation range, we put it on our short list for further evaluation

If we identify Key Thesis Points™ (long-term catalysts) unique to that company that we believe will improve fundamentals, and we think the reward/risk ratio is at least 3/1, we may purchase the name in the portfolio.

Deep Value

We constantly scour the market in areas that have been sold off. There are many ways that contrarian opportunities present themselves.

If a company reaches our valuation qualification and passes our balance sheet criteria, we put it on our “short list” for further evaluation.

After further review, if we identify Key Thesis Points™ (long-term catalysts) unique to that company that we believe will improve fundamentals and the reward/risk ratio is at least 3/1, we may purchase the name in the portfolio. We seek opportunities with significant upside for the Deep Value Sleeve of the portfolio.

We will replace a name for a significantly better reward/risk opportunity.

Change in Thesis

If new information suggests we have made a mistake or Key Thesis Points™ is broken, we will immediately liquidate the position.

Trimming

If a position becomes too large or the reward/risk ratio is less favorable, we will likely trim it down.

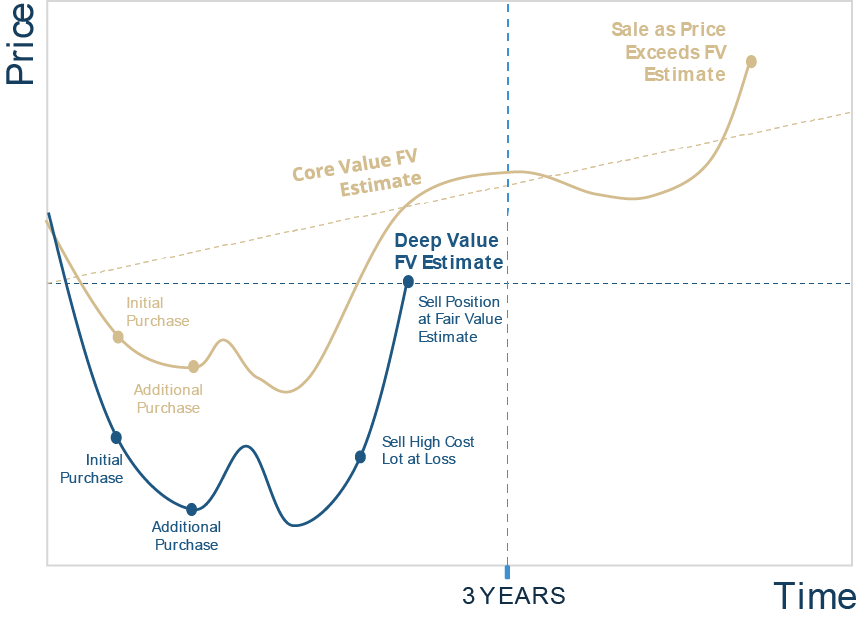

Valuation

Deep Value names are sold at fair value estimates. Core Value holdings are sold based on valuation alone only when we believe they are significantly stretched.

Tax Efficiency is a Byproduct of our Disciplined Process

The visual shown above is for illustrative purposes only and does not guarantee a certain level of performance or success. Not all investments will reach or exceed their estimated fair market value. Investors can lose all or part of their money.

Buy & Hold

Longer holding periods are inherently more tax efficient.

Strategy Implementation

We maintain a contrarian discipline of buying out of favor stocks. Generally we make a small initial purchase (1-2%) with anticipation of further price declines and additional buying opportunities. Dollar cost averaging produces a variety of tax lots. As stocks rebound toward fair value estimates, higher cost lots offset embedded gains, leading to a more tax efficient portfolio.

While low tax implications are not the main focus of the strategy, they tend to be a by-product of our disciplined buy/sell process. The mutual fund vehicles of our strategies illustrate the tax efficiency. (see mutual fund distribution history for more information)

We use cookies to improve your experience on our site. To find out more, read our privacy policy and cookie policy. By continuing to browse this site, you agree to our use of cookies.